Strengthening Accountability for Recover Forward

How Supreme Audit Institutions advance sustainable development

In many countries, the COVID-19 pandemic and other crises, including most recently the sharp increases in food and energy prices triggered by Russia’s war on Ukraine, have caused havoc to fiscal policies in several ways. During the pandemic, economic development slowed down or came to a halt, leading to revenue losses for governments. Moreover, short-term public sector emergency spending to counterbalance the adverse impact of the pandemic on the population and across sectors as well as higher spending on awareness and vaccination campaigns led to further increases in fiscal deficits. As the pandemic is receding, big recovery spending packages are being initiated that tend to widen fiscal deficits even further while often resulting in higher government indebtedness. More generally, the COVID-19 pandemic has eroded previously achieved progress in poverty reduction, widened inequality within and across countries and threatens the achievement of the Sustainable Development Goals (SDGs) by 2030. Fiscal pressures have been heightened more recently by sharp increases in food and energy prices, triggered by Russia’s war on Ukraine. These are fuelling inflation and hampering economic recovery, while adding fiscal pressures through higher spending by governments, including for subsidies and compensation packages for population groups and businesses.

These adverse impacts of the multiple crises are keeping many poorer countries around the world in tight grip, and they have exacerbated previously existing structural problems in fiscal policies. These include low levels of revenues, weak tax administrations, inadequacies in public service delivery, including in social expenditure programmes that do not sufficiently focus on needy population groups, wasteful subsidies, inadequate financial control mechanisms, procurement, and public investment programming and management. In many countries of the developing world, the pandemic thus exposed weaknesses in fiscal management, while putting pressure on governments to increase spending in a bid to at least seek to dampen the worst impacts of the COVID-19 crisis on poverty and inequalities.

These crises, however, also present an opportunity. Key opportunities for fiscal reforms and further efforts to fight the impacts of the COVID-19 pandemic and other crises should start by reflecting on the exposed weaknesses in fiscal management, then identifying key bottlenecks, and finally redoubling efforts to implement reforms to improve fiscal management. Fiscal reform efforts should strive to recover better in the sense of, making spending more focused on the alleviation of poverty and inequalities, while also addressing ecological concerns and challenges from climate change, hopefully yielding environmentally more sustainable, greener spending trajectories. A new wave of fiscal reform efforts seems needed in many countries to overcome the adverse impacts of the COVID-19 pandemic, resulting also in renewed and strong progress towards achieving the SDGs by 2030.

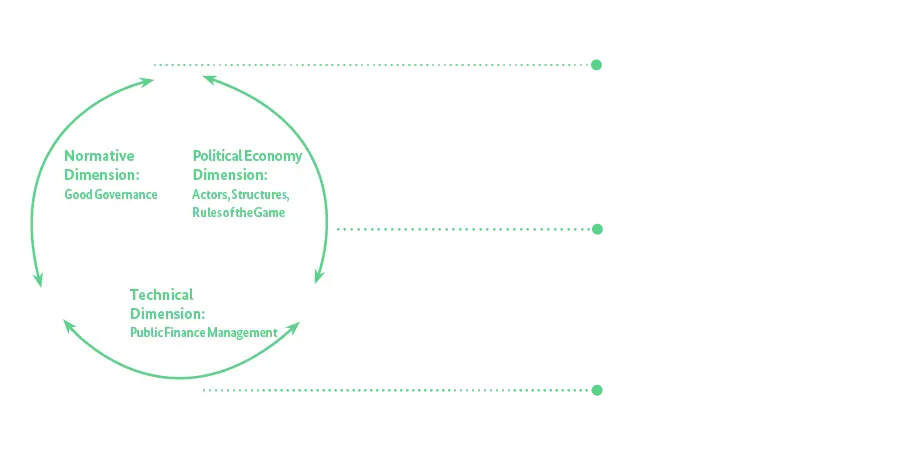

The German development cooperation takes a holistic view of fiscal policy, incorporating the normative and political-economy dimensions of policy formulation in addition to the technical dimension. Consequently, Good Financial Governance focuses on reducing poverty and inequality through fair, accountable, and transparent public financial management systems. Within this strategic approach, six main technical areas are identified: creating fair, transparent and efficient tax systems; redistributive and fair public expenditure management; using procurement systems; fiscal decentralisation; debt management; and accountability for the use of public funds.

The following topics highlight specific fiscal policy challenges that have been identified by German development cooperation as key areas of support as well as relevant resources to recover forward after the COVID-19 pandemic and other crises:

How Supreme Audit Institutions advance sustainable development

Governments worldwide have taken unprecedented measures to respond to the COVID-19 pandemic and its economic and social impacts. To a lesser degree, they also try to compensate consumers for higher energy and food prices that result from the war in Ukraine. Governments have to balance the need for a quick response with the need to comply with established procedures that ensure efficiency, transparency, and value for money in the use of public resources. Emergency procedures in public procurement, for example, have in many cases been tainted with accounts of misuse of funds and corruption. Economic stimulus packages and other Recover Forward measures provide large amounts of public resources for specific objectives that need to be spent efficiently and effectively to achieve their goals.

Supreme Audit Institutions (SAIs) are key to ensuring accountability for the use of public funds in the response to COVID-19, consequences of the war against Ukraine and the subsequent recovery phases. SAIs are established as independent oversight bodies with a mandate to undertake financial, compliance and performance audits to hold governments to account and issue specific recommendations for improvement, thus complementing other accountability institutions and actors (e.g., parliaments, civil society, and the media) and governments’ internal audit, monitoring and evaluation systems.

Thus, they have an important role in fostering sustainable development and the realisation of the 2030 Agenda in the German development cooperation’s partner countries. The 17 SDGs provide an ambitious set of targets for all member states of the United Nations, which are accompanied by a detailed monitoring framework to track their progress. SAIs can provide advice, assurance and assessment on the preparation, implementation, monitoring and reporting on progress of the SDGs. The International Organisation of Supreme Audit Institutions (INTOSAI) has recognised the relevance of the 2030 Agenda for SAIs worldwide since its adoption.